Modern Portfolio Theory (MPT) has been introduced in 1952 by Markowitz. As described in Wikipedia, "MPT is a theory of finance that attempts to maximize portfolio expected return for a given amount of portfolio risk, or equivalently minimize risk for a given level of expected return, by carefully choosing the proportions of various assets. Although MPT is widely used in practice in the financial industry and several of its creators won a Nobel memorial prize for the theory, in recent years the basic assumptions of MPT have been widely challenged by fields such as behavioral economics.

MPT is a mathematical formulation of the concept of diversification in investing, with the aim of selecting a collection of investment assets that has collectively lower risk than any individual asset. This is possible, intuitively speaking, because different types of assets often change in value in opposite ways. For example, to the extent prices in the stock market move differently from prices in the bond market, a collection of both types of assets can in theory face lower overall risk than either individually. But diversification lowers risk even if assets' returns are not negatively correlated—indeed, even if they are positively correlated.

More technically, MPT models an asset's return as a normally distributed function (or more generally as an elliptically distributed random variable), defines risk as the standard deviation of return, and models a portfolio as a weighted combination of assets, so that the return of a portfolio is the weighted combination of the assets' returns. By combining different assets whose returns are not perfectly positively correlated, MPT seeks to reduce the total variance of the portfolio return. MPT also assumes that investors are rational and markets are efficient."

Since 1952 the world has changed. It has changed even more in the past decade, when complexity and turbulence have made their permanent entry on the scene. Turbulence and complexity are not only the hallmarks of our times, they can be measured, managed and used in the design of systems, in decision-making and, of course, in asset portfolio analysis and design.

Assetdyne is the first company to have incorporated complexity into portfolio analysis and design. In fact, the company develops a system which computes the Resilience Rating of stocks and stock portfolios based on complexity measures and not based on variance or other traditional approaches. While conventional portfolio design often follows the Modern Portfolio Theory (MPT), which identifies optimal portfolios via minimization of the total portfolio variance, the technique developed by Assetdyne designs portfolios based on the minimization of portfolio complexity. The approach is based on the fact that excessively complex systems are inherently fragile. Recently concluded research confirms that this is the case also for asset portfolios.

Two examples or Resilience Rating of a single Stock are illustrated below:

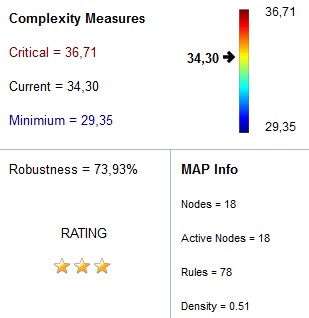

An example of a Resilience Rating of a portfolio of stocks is shown below (Top European banks are illustrated as an interacting system):

while the rating and complexity measures are the following:

The interactive map of the EU banks may be navigated on-line here.

For more information, visit Assetdyne's website.

No comments:

Post a Comment